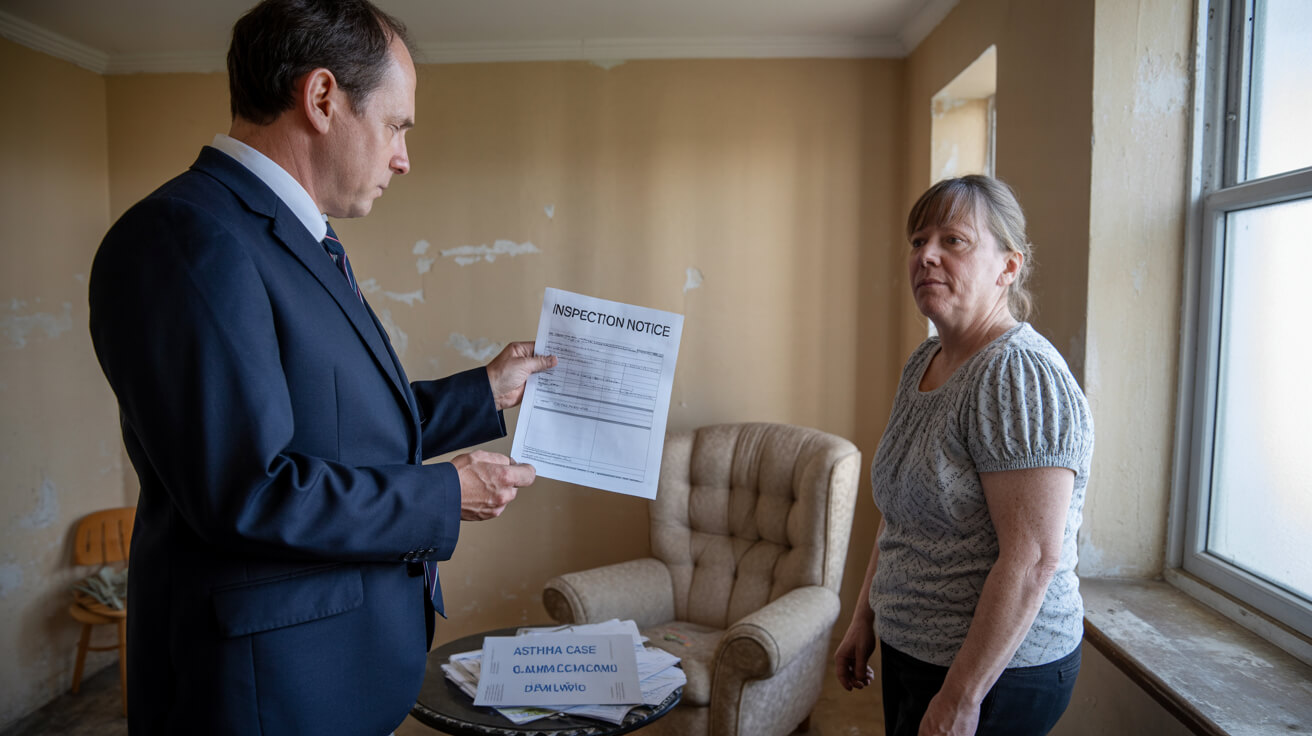

FRA Closure PPM Services for Lenders – Fire Risk Assessment Action Evidence & Mortgage Approval

For lenders, brokers, managing agents and block owners facing stalled mortgage or remortgage cases, FRA closure PPM turns open fire risk assessment actions into clear, lender-ready evidence. Each FRA finding is mapped to works completed, dates, ownership, verification and residual risk, depending on constraints. You end up with a structured, decision-ready register that valuers, underwriters and conveyancers can follow without chasing scattered emails or unclear records. When you are ready to move cases forward with fewer fire-safety queries, this is the process to rely on.

Author

Izzy Schulman

When mortgage or remortgage cases stall after a fire risk assessment, the problem is often missing closure evidence rather than the FRA itself. Lenders, valuers and conveyancers need to see what was done about each material action, not just that risks were identified.

FRA closure PPM services from All Services 4U organise that story into a structured register that links findings, remedial works, dates, responsible parties and verification. This gives lender-facing teams a clearer file, stronger trust signals and fewer repeat queries during valuation, underwriting and legal review.

- Connect each FRA action to clear, dated evidence

- Show closure, control and governance in a lender-friendly format

- Reduce repeat fire-safety queries and help cases progress</p>

Need Help Fast?

Locked out, leak at home, or electrical issue? All Services 4 U provides 24/7 UK locksmith, plumbing, electrical.

Testimonial & Clients Who Trust Us

With 5 Star Google Reviews, Trusted Trader, Trust Pilot endorsements, and 25+ years of experience, we set industry standards for excellence. From Dominoes to Mears Group, our expertise is trusted by diverse sectors, earning us long-term partnerships and glowing testimonials.

Worcester Boilers

![]()

Glow Worm Boilers

![]()

Valliant Boilers

![]()

Baxi Boilers

Ideal Boilers

FRA closure PPM services for lenders: what the service is designed to evidence

FRA closure in a lending context means proving what happened after the Fire Risk Assessment, not just producing the report.

You are trying to move live mortgage or remortgage cases through valuation, underwriting and legal review without repeated fire‑safety queries from the mortgage lender. To do that, you need a file that shows, for each material FRA action, what was wrong, what was done, when it was done, who did it, and how closure was checked. That is the gap FRA closure planned‑preventive‑maintenance (PPM) services are designed to fill.

Instead of a narrative assessment and scattered emails, you end up with a structured register: one row per action, with a named owner, status, target date, required evidence and verification point. If an FRA identifies non‑compliant flat entrance doors on three floors, the register should show which doors are affected, when each was replaced, and the commissioning record for the new doors, all tied back to the original finding. A reviewer can then see at a glance which items are genuinely closed, which are in progress and which still influence value, insurability or saleability.

This is not a replacement FRA. The assessment remains your starting point. The service sits on top of it and shows how you have completed, controlled or explicitly left open each recommendation in a way a lender can understand.

All Services 4U delivers this as a lender‑aware closure and evidence process, so your fire‑safety story is documented for decision‑makers rather than only for internal compliance files.

Why an FRA alone may not satisfy a mortgage lender

An FRA can identify risk, but it rarely proves that the risk has been resolved or is being managed over time.

From a lender’s point of view, a dated FRA that lists medium and high‑priority actions tells them there was a problem, not that it has gone away. A managing agent saying that “works are in hand” describes intent, not outcome. Until there is evidence that actions are complete or credibly controlled, the building still sits in a higher‑risk bucket.

Conflicting documents make this worse. If different reports and certificates use inconsistent dates, descriptions or severity ratings for the same issue, legal and valuation teams have to slow down while they work out what to rely on. A single unresolved item can then cast doubt on the overall governance of the block.

Lenders are also weighing cost and marketability. Where actions touch external walls, compartmentation or major life‑safety systems, they are thinking about potential remediation spend, who bears that spend, and whether any of it could undermine value or future saleability.

In practice, when a case stalls after an FRA, it is usually because the file does not yet tell a clear “before and after” story. The missing piece is structured post‑FRA evidence, not more copies of the assessment.

FRA reports show findings; lenders need closure and control

Your FRA is still essential. It shows you understand the building and have identified hazards. For a mortgage decision, though, reviewers want to see three extra layers:

- which actions are now closed, with proof

- which remain open but are actively controlled, with interim measures described

- who is overseeing the remaining work and on what timetable

Which fire safety issues most often hold up lending decisions

Some FRA actions cause far more lending friction than others because they drive both safety concerns and uncertainty about future cost.

When you triage a long action list against mortgageability, the defects that usually need attention first are: external wall concerns, compartmentation failures, flat entrance and common‑area fire doors, alarm and detection faults, emergency lighting issues and weaknesses in smoke control or ventilation.

High‑impact defects and why they worry reviewers

Compartmentation and door issues matter because they underpin your fire strategy. Repeated breaches, poorly performing doors, or unclear locations make it harder for a valuer to be confident that stay‑put or evacuation arrangements will work as intended. That often leads directly to referrals or qualifications on the valuation.

External wall matters remain especially sensitive. Where cladding, balconies, insulation or attachments raise questions, they tend to combine technical uncertainty, remediation cost, funding responsibility and reputational risk. That is why cases involving external walls usually attract additional evidence requests.

Repeated faults on alarms or emergency lighting are read as governance signals, not just technical glitches. If tests are regularly failing or certificates are patchy, a lender can reasonably ask whether other controls are also weaker than they appear on paper.

Prioritising actions for a lender‑facing file

When you prepare a file for review, it helps to rank actions by:

- effect on life safety if the defect persists

- likely impact on value, insurance and service‑charge exposure

- quality and clarity of evidence currently on file

What lenders, valuers and conveyancers usually need to see

Review teams want enough information to reach a defensible view on safety, value and residual risk without rebuilding the story from raw documents.

Their starting question is simple: “Can we see the current risk position and remedial status clearly enough to support a lending decision?” If the answer is no, the default response is delay, further enquiries or a cautious lending stance.

The emphasis on evidence, not reassurance

In practice, the most useful records are dated and traceable. They connect:

- the original FRA finding or defect

- the work that was done, with scope clearly defined

- the competent person or firm that carried it out

- the checks or commissioning used to confirm it now performs correctly

Residual risk wording then explains what, if anything, remains open, what interim measures are in place, and what further decisions or works are still anticipated.

For conveyancers, the summary must separate closed, partially complete and unresolved items in clear language that can be reported back to the lender. For valuers and case handlers, competence and reliance matter: they will look at who signed each element, whether that person was appropriate for the task, and how far they can rely on the conclusion.

What a lender‑ready FRA action evidence pack should contain

A lender‑ready evidence pack is a compact, indexed bundle that shows how you manage fire‑safety risk from assessment through to close‑out.

At minimum, you want the latest FRA, the original action list, a live tracker and a dated schedule that distinguishes closed items from those still in progress. That becomes the backbone of the story.

From actions to proof: linking each item to one primary record

For every material action, aim to be able to point to one primary supporting record. That might be a completion sheet, a commissioning certificate, a marked‑up plan, a survey extract or before‑and‑after photographs. The key point is that a reviewer can move from “this was the issue” to “this is the evidence that it was resolved or controlled” without guessing.

Version control underpins trust. If document titles, dates and revision histories do not line up across the pack, confidence in the whole file suffers, even if the underlying work is sound.

Handling open items without undermining the pack

You do not need to hide open actions from a lender. You do need to label them precisely. For each one, show:

- current status

- interim controls in place

- target dates

- known dependencies, such as access, funding or statutory approvals

Be clear where you rely on technical certification, where you rely on management confirmation, and where both are present. That clarity helps reviewers judge how far they can safely rely on each element.

How a PPM‑led closure process turns FRA actions into auditable evidence

A planned‑maintenance‑led approach bakes evidence and accountability into the way you close FRA actions, instead of trying to bolt them on afterwards.

If your current challenge is that teams are constantly chasing proof once works finish, you benefit from defining the closure process up front. That means specifying, for every action, who owns it, when it should be done, what access is needed, what work is expected, what evidence must be returned, and who will review that evidence.

When existing contractors are already in place, you do not necessarily need to replace them. You do, however, need to adjust instructions so that completion records, photos and verification steps are treated as deliverables, not as extras if time allows.

For clusters of actions, a single, well‑maintained register showing dates, responsibilities and document locations becomes your audit trail. That register in turn drives the evidence pack, rather than someone having to reconstruct history from inboxes and ad‑hoc folders.

From a lender’s perspective, a repeatable closure method signals control. It shows that evidence was captured during delivery and that the pack reflects live records, not memory or retrospective narrative.

All Services 4U’s FRA closure PPM model is built around that principle: every significant action is routed through a clear workflow so the evidence you need later is created and filed as the work is done.

Accreditations & Certifications

What this does and does not mean for mortgage approval

Stronger FRA closure evidence reduces uncertainty for lenders, but it does not override lending policy, valuation or legal reporting.

You should expect that a well‑prepared pack will reduce avoidable delay, cut back on repeated questions, and support a more confident view of the building. You should not assume it will, on its own, guarantee a particular lending outcome.

Documentation cannot turn unfinished remediation into completed work. Where actions are still open, the most responsible course is to present them honestly, describe the controls in place and set out the planned next steps. That transparency allows reviewers to decide whether residual risk and cost exposure fit within their appetite.

For higher‑risk buildings – for example those with complex façades, significant height or wider building‑safety cost issues – decisions will still be influenced by broader legal, regulatory and market factors. A good FRA closure pack helps those factors be weighed on clear facts rather than on speculation.

When stakeholders are under chain or refinance pressure, it is tempting to over‑promise. Your role is to support an informed lending decision with clear, defensible evidence, not to promise certainty where the market cannot provide it.

Reliable Property Maintenance You Can Trust

From routine upkeep to urgent repairs, our certified team delivers dependable property maintenance services 24/7 across the UK. Fast response, skilled professionals, and fully insured support to keep your property running smoothly.

Book your free consultation with All Services 4U today

A short, structured conversation is often the quickest way to stabilise a case and understand what evidence is really missing. Book that call before the next valuation round, not after a file has already been queried.

On an initial call, you can walk through your latest FRA, any existing action tracker, key certificates and the specific questions the lender, valuer or conveyancer has raised. The aim is to move from a vague sense of “we keep being asked for more” to a concrete map of what already evidences closure, what is only partially supported, and what still needs work.

To keep that discussion productive, it helps if you have:

- the current FRA and action list

- any live status register

- available completion records and certificates

- copies of the latest lender or solicitor queries

From there, we can suggest whether you need a focused gap analysis, a managed close‑out programme, or a cleaner, lender‑facing evidence file built from records you already hold.

If remediation is still in progress, the consultation can still separate fact from assumption so you present the building’s position accurately rather than optimistically. The next step should be a practical action list: who will supply which documents, which actions should be prioritised, and how the final pack will be assembled.

Schedule a consultation now and put a clear FRA closure and PPM plan around your building so your next mortgage or remortgage case can move on a properly evidenced basis.

Frequently Asked Questions

What evidence moves an FRA action from open item to lender-reliable closure?

An FRA action becomes lender-reliable when the record shows completion, verification, and current status in one traceable chain.

A Fire Risk Assessment can identify a defect. It does not, by itself, prove that the issue was corrected, checked, and brought under control in a way a lender, valuer, or conveyancer can rely on. That is where many refinance and sale files begin to slow. The real test is not whether your team discussed the action. It is whether the file shows a clean line from finding, to remedial work, to review, to present position.

For most residential blocks, the strongest approach is a controlled action file. Each material item should connect the original FRA reference to the scope of work, the contractor or specialist involved, the completion date, the supporting evidence, and the person who accepted closure. UK Finance expectations matter here because lenders are trying to judge whether the building can be understood with confidence, not whether the paperwork sounds reassuring.

A closed action is not a promise. It is proof that still makes sense under pressure.

In practice, weak files usually fail in the joins. One document says works were done. Another proves somebody attended. A third suggests the issue is no longer live. But if those records do not align against the same action reference and status line, the file still reads as uncertain. That uncertainty creates cost. It slows legal review, complicates valuation language, and invites more lender follow-up.

What should a close-out record contain for each FRA action?

A useful stress test is simple: could an independent reviewer understand one action in under two minutes? If they need to search across inboxes, unnamed photos, or conflicting tracker versions, the evidence is still too loose.

A dependable close-out record usually includes:

- the exact FRA action wording or reference number

- a short note stating what was done

- a dated completion point

- visual or technical confirmation

- the name and role of the person accepting closure

From a lender or valuer perspective, that structure matters because it reduces interpretation. The reviewer is not trying to reward effort. They are trying to understand the current state of the risk.

What does weak FRA closure evidence usually look like?

Weak evidence often shows activity without verification. Typical examples include:

- invoices with no matched action reference

- photos with no date, location, or sequence

- a tracker updated to “complete” without supporting proof

- a management email saying “resolved” without technical backing

In a remortgage file, those gaps create drag because the reviewer has to infer too much. The Law Society’s building safety guidance matters for that reason. Conveyancers are expected to report material issues properly. If the evidence is incomplete, the process usually gets slower rather than more forgiving.

How should your team prove technical closure rather than administrative closure?

The strongest files separate three layers clearly:

| Layer | What it proves | Typical evidence |

|---|---|---|

| Completion | The work happened | work records, dated attendance, photos |

| Verification | The result was checked properly | survey, test record, commissioning, review note |

| Status | The item is now closed or still live | action register, owner, closure date |

That distinction is especially useful where the original action involved alarms, emergency lighting, fire doors, or compartmentation. A completed job note may show attendance. It may not show that the defect no longer affects the building’s fire strategy. Where relevant, standards such as BS 5839, BS 5266, and BS 8214 help frame what good verification should look like.

Why does this matter for boards, managing agents, and refinance teams?

For an RTM director or RMC chair, the gain is board confidence. You can see what is actually discharged, what still needs budget or access, and what would withstand challenge if a sale or remortgage lands without warning.

For a managing agent or maintenance lead, the gain is speed. Your team spends less time rebuilding history from scattered records and more time submitting a controlled position.

For a lender-facing file, document order matters more than document volume. If your current close-out records do not make that chain obvious, a lender-ready closure review can show whether you need more works, better indexing, or both. That is often a faster route to refinance readiness than another round of broad reassurance.

Why do mortgage and remortgage cases still stall when FRA works are already under way?

Because works in progress still read as live risk until the present position is documented clearly and defensibly.

This is one of the most common misunderstandings in residential property compliance. Your team may have instructed works, raised orders, arranged access, and started remediation, yet the refinance or sale still pauses. From the lender’s side, that is not unreasonable. A live programme can still mean uncertainty over safety, cost, programme risk, and marketability. Operational progress matters. Credit and valuation confidence matters more.

The issue is often not the works themselves. It is the fragmented story around them. The contractor has photographs. The managing agent has a tracker. The fire consultant has the original wording. The board has partial updates. The conveyancer has a deadline. The lender receives fragments instead of one controlled position.

Why is “works instructed” too weak for most lender reviews?

A lender-side reviewer usually wants four answers fast:

- what remains open today

- what has been completed

- who has checked the result

- what controls are in place while live items remain

Until those points appear in one place, “works instructed” can sound like movement without resolution. The Law Society guidance is relevant because conveyancers are not there to smooth over uncertainty. They are there to report it accurately.

A better belief to work from is this: many teams assume delay means the lender wants more documents. Often the lender wants a cleaner status picture. That means a submission that separates completed items from live ones, explains dependencies plainly, and shows what protects the building in the meantime.

How does live FRA work affect different stakeholders?

For a property manager, delay usually shows up as repeated lender queries and impatient leaseholders. For an asset manager, it appears as valuation uncertainty and disposal friction. For a finance lead, it can threaten refinancing windows and covenant assumptions. For a board member, it becomes a governance problem because no one can answer a direct question simply.

In practice, a stronger present-position file should show:

- discharged actions

- partially complete actions

- outstanding actions

- interim measures linked to each open risk where needed

That format helps everyone stop talking past one another.

How should your team present live FRA works without weakening the case?

A stronger submission does not pretend everything is finished. It does something more useful. It identifies live items, shows current stage, names the dependency, and records the interim measure. RICS commentary matters here because valuers do not react only to defects. They react to uncertainty around defects.

If fire door replacements are commissioned but not fully signed off, a useful submission distinguishes between surveyed defects, ordered replacements, completed installations, and flats awaiting access. If alarm defects are under remediation, the file should show service history, fault history, interim monitoring, and the date of the next verification step.

That kind of sequencing is simple, but it changes the commercial effect of the file. It turns a messy update into a controlled one.

What makes a case move faster once works are already live?

From a valuer’s perspective, confidence comes from knowing what remains uncertain and what has already been stabilised. For a conveyancer, it comes from having facts that can be reported without guesswork. For a lender, it comes from seeing active management rather than reactive explanation.

The practical gain is fewer follow-up questions, cleaner legal review, and less board time spent reconstructing what happened. If your team is already mid-case, a present-position review usually does more than another broad progress note. Where refinance timing matters, a lender-ready status pack can be the difference between a controlled delay and an avoidable one.

Which FRA actions are most likely to delay valuation, approval, or refinance?

The actions that delay lending most are the ones that affect life safety, marketability, or future cost in visible ways.

Not every FRA item carries the same lending weight. Minor housekeeping issues are one thing. Defects that raise questions about compartmentation, fire doors, alarms, emergency lighting, external walls, or management control are another. These are the issues that attract scrutiny because they affect both resident safety and commercial confidence in the building.

External wall concerns usually sit near the top because they combine technical uncertainty, potential remediation cost, responsibility questions, and saleability risk. Internal deficiencies matter as well. If a reviewer sees repeated alarm faults, incomplete fire-stopping, or poor fire door records, they may conclude the issue is wider than the single defect on the page. RICS commentary is important here because valuation is shaped by uncertainty as much as defect type.

Which FRA-related defects tend to trigger the most lender queries?

A practical hierarchy often looks like this:

| Defect type | Why it slows lending | What usually helps review move |

|---|---|---|

| External wall concerns | cost, safety, and saleability uncertainty | competent assessment, clear status, funding position |

| Compartmentation breaches | confidence in fire strategy is weakened | survey evidence, remedial proof, verified close-out |

| Fire door defects | escape protection and containment concerns | inspection records, remedial evidence, replacement history |

| Alarm or emergency lighting failures | weak maintenance control is implied | BS 5839 or BS 5266 records, service logs, closure evidence |

That hierarchy matters because it helps your team focus effort where it changes the transaction outcome. Too many teams chase the easiest contractor response rather than the issue doing the most damage to lender confidence.

Which open actions should be prioritised first when the tracker is long?

The most effective order is usually:

- highest safety consequence

- highest valuation sensitivity

- weakest current proof

- greatest likelihood of repeat lender questions

That means a poorly evidenced external wall item may deserve attention before a cleaner low-impact housekeeping point. The Building Safety Act has also increased the value of traceability. Even where the higher-risk regime does not apply in full, reviewers respond better to records that feel structured rather than improvised.

What makes a building look weakly controlled to a valuer or lender?

In practice, weak management control looks like ad hoc updates, partial contractor notes, and trackers that do not match their evidence. A stronger control picture shows routine testing, dated remedials, named accountability, and files that agree with one another.

For a compliance lead, that affects how quickly queries can be answered. For a board member, it affects how defensible oversight looks. For an asset or finance lead, it affects whether uncertainty starts to influence valuation assumptions.

How should your team decide what to fix or package first?

Start with the items that combine high consequence and low proof quality. Build a short list of three or four actions most likely to influence mortgageability now. Then ask what is missing for each one:

- technical confirmation

- current photographs

- commissioning or test records

- an updated specialist review

- better-ordered close-out evidence

That kind of triage usually saves more time than a broad request for “all FRA documents”. For portfolio teams, it also shows where the true exposure sits and where the problem is simply poor file control. If you need to prepare a refinance-sensitive block quickly, an FRA closure audit from All Services 4U can help identify which live actions are genuinely slowing lender confidence and which ones only need stronger evidence order.

How should an FRA action file be structured for lenders, valuers, and conveyancers?

The most useful FRA action file is concise at the front, evidence-led at the back, and easy to audit throughout.

A lender-facing FRA file should not read like a technical dump. It should read like a controlled submission that answers obvious questions before anyone has to ask them twice. The front should explain the current position. The back should prove it. That balance is where many otherwise competent teams lose credibility.

A strong file usually opens with a short building summary, the material fire-safety issues, the current status of those issues, and any live residual risks. It then moves into an indexed action register and evidence appendices arranged by action reference. Building Safety Act discipline matters because traceable information increasingly shapes how even standard residential files are received.

How should the front of the file be arranged?

The opening section should help a lender, valuer, or conveyancer understand five things quickly:

- the building context

- the material actions raised

- what is closed

- what remains live

- what interim controls apply

This is not where caveats should be buried. A precise open issue is usually less damaging than an overconfident statement that later falls apart.

From a conveyancer’s perspective, the front of the file should make current position clear enough to report. From a board perspective, it should show whether risk is under control. From a lender perspective, it should remove the need to interpret scattered attachments.

A practical file order usually works best when it follows a fixed sequence:

- Building summary — current position and material issues

- Action register — one line per action with status, owner, and date

- Closure evidence — reports, photos, certificates, commissioning, sign-off

- Open-item notes — dependencies, interim controls, next review dates

That layout helps different reviewers do different jobs quickly. Valuers can see where uncertainty still sits. Conveyancers can report what is current. Lenders can decide whether the file is controlled.

Which common filing mistakes weaken otherwise good FRA records?

Several errors show up repeatedly:

- duplicate trackers with different statuses

- unnamed photo folders

- undated screenshots

- consultant reports with no linked action number

- summary pages that blur closed and open items

Once status becomes blurred, every appendix becomes less persuasive. A stronger file avoids volume for its own sake. It aims for one action, one path, one proof set.

What would a stronger file structure look like in practice?

If an FRA identified deficient fire doors, the summary should state how many doors were affected, how many were remediated, whether follow-up inspection occurred, and whether any flats remain outstanding due to access. The appendices should then let a reviewer test that statement quickly through survey extracts, contractor records, photographs, and competent sign-off.

For teams handling repeated lender enquiries, that sort of structure does more than tidy the file. It reduces repeat administration. It also signals that the building is managed through routine oversight rather than inbox archaeology. If your board or broker keeps asking for the same supporting records in different formats, a lender-pack diagnostic with All Services 4U is often a practical way to standardise the file before the next transaction window.

Who should sign off FRA action closure, and when does a management letter stop being enough?

Closure carries more weight when the sign-off matches the defect, the work completed, and the competence needed to verify it.

There is no single signature that closes every fire-safety issue properly. A management letter can help explain status, file order, and current controls, but it rarely stands on its own where the defect depends on specialist judgement, regulated work, commissioning, or updated inspection. The real question is straightforward: who says this issue is closed, and why are they the right person to say it?

That is where many files weaken. A managing agent may be the right party to explain record maintenance and status tracking. They are not always the right party to replace technical verification. The National Fire Chiefs Council has consistently supported clearer accountability and stronger management evidence. In lending terms, that means a file becomes more persuasive when operational completion and appropriate technical sign-off sit together.

When does a management letter add value?

A management confirmation helps when it does three jobs well:

- confirms the current register status

- explains how records are maintained and indexed

- states what remains open and what interim controls apply

That kind of letter supports the file because it shows active oversight. It tells the reviewer there is management control, not just document storage.

When is a management letter too weak on its own?

A management letter usually becomes too thin where the issue depends on:

- commissioning or re-testing

- specialist inspection findings

- regulated completion evidence

- fresh technical review of residual risk

A statement that emergency lighting defects were resolved may not carry much weight without logs or duration test confirmation. A note saying fire doors were addressed will feel soft if it is not backed by survey evidence, remedial proof, or competent sign-off. The same applies to alarm reliability, compartmentation, and external wall concerns.

How should closure sign-off be matched to the defect type?

A practical way to structure sign-off is in three layers:

| Layer | Question answered | Typical sign-off source |

|---|---|---|

| Completion | Was the work carried out? | contractor or installer |

| Verification | Was the result checked properly? | competent specialist, inspector, or tester |

| Oversight | Is the register now accurate and current? | managing agent, compliance lead, or accountable role |

That format gives the file more resilience. It also makes it easier for boards, lenders, and conveyancers to understand what kind of confidence sits behind the closure statement.

What does this mean operationally for your team?

It means management explanation should support technical records, not try to replace them. A good management note can improve confidence. A weak one can highlight the absence of harder proof.

That becomes more important across a portfolio. If your team is producing lender packs for multiple blocks, matching sign-off to defect type will reduce repeated questions about who actually confirmed closure. The commercial gain is simple: fewer email chains, faster review, and less board time spent defending records that should have been stronger in the first place.

If your current packs rely too heavily on generic management wording, a closure-signoff review can help identify where technical verification needs to be strengthened before the next lender or valuer query lands.

How do planned FRA close-out services reduce repeat lender queries after one case has already moved?

They reduce repeat lender queries by replacing one-off remediation proof with an ongoing, lender-readable control record.

Many teams treat mortgage friction as a one-case problem. Once the mortgage lender stops asking questions, the pressure drops and everyone moves on. The weakness appears later. The next buyer, valuer, broker, insurer, or board member asks the same questions again. If the building only has a rescue file assembled under pressure, your team pays twice: once to solve the issue, and again to rebuild the record.

Planned close-out services change that pattern. Instead of proving that something was fixed once, the building starts to show that testing, inspection, maintenance, and remedial follow-through now sit within a live control process. The Fire Industry Association has long emphasised planned maintenance as the basis for sustained system performance. In lender language, continuity of control is usually more reassuring than a late-stage bundle of historic documents.

How does a planned close-out approach help after the first transaction?

It turns the file from reactive to repeatable. Instead of scrambling every time someone asks for proof, your team can point to:

- one live action register

- standard close-out requirements by defect type

- current servicing and testing records

- scheduled follow-up checks

- periodic file reviews before renewal or refinance

That gives future reviewers less reason to wonder whether the building is only managed when a transaction forces attention.

What does a repeatable close-out process look like in practice?

Take recurring alarm faults or repeated emergency-lighting failures. A one-off response may prove that a single issue was fixed in one month. A planned close-out service shows inspection dates, service history, remedial history, follow-up verification, and the current operating position. That creates a different level of confidence.

For a managing agent, that means fewer repeated evidence hunts. For a board, it means clearer oversight. For an asset or finance lead, it means less transaction drag the next time refinancing, disposal, or insurance review comes around.

Why does this matter commercially as much as operationally?

Repeat queries create hidden cost. Staff lose time rebuilding files. Contractors get dragged back into old issues. Boards receive vague updates instead of clear positions. Insurers and lenders begin to read the building as harder work than it should be.

A planned close-out model reduces that drag because evidence capture becomes part of ordinary control rather than a late-stage scramble. The practical gain is fewer lender follow-ups, quicker legal review, and better board assurance. That is especially useful across portfolios where the same weaknesses tend to repeat from block to block.

When is it worth moving from ad hoc close-out to a planned service?

Usually earlier than teams expect. If you are handling multiple blocks, recurring lender questions, or repeated board requests for the same supporting records, the value appears quickly. One representative building is often enough to prove the benefit. Once your team sees how much time disappears into repeated evidence reconstruction, a controlled close-out workflow starts to look less like admin and more like asset protection.

If you need the next refinance, insurer review, or board submission to move with less friction, a planned FRA close-out service from All Services 4U can help convert one-off remediation proof into an ongoing control record that already knows how to answer the next question.

- FRA closure PPM services for lenders: what the service is designed to evidence

- Why an FRA alone may not satisfy a mortgage lender

- Which fire safety issues most often hold up lending decisions

- What lenders, valuers and conveyancers usually need to see

- What a lender‑ready FRA action evidence pack should contain

- How a PPM‑led closure process turns FRA actions into auditable evidence

- What this does and does not mean for mortgage approval

- Book your free consultation with All Services 4U today

- Frequently Asked Questions

- Related PPM Services

Case Studies

Related Articles

Your Guide To Identifying And Treating Minor Mould Outbreaks

Why Planned Preventative Maintenance (Ppm) Saves Money And Ensures Compliance